Smart Investing Made Simple: The Power of an Integrated Investment Plan

Smart investors constantly search for financial products that deliver both safety and growth potential. The Securities and Exchange Board of India (SEBI) is developing an

Similar to other insurance policies, a life insurance policy functions in a manner that the policyholder must pay a premium for a set period of time. After the death of the insured person, the insurance company will cover the financial needs of the insured’s family. The amount to be paid by the insurance company will depend upon the premium the insured person paid to the company.

Let’s understand life insurance with a simple example:

Mr. Wilson wants to protect his family in case of his early death. So, he buys a 20-year life insurance policy with a premium of Rs. 15,000 per year. If Mr. Wilson dies within the 20-year term, the insurance company will pay his family the beneficiary amount of Rs. 15,00,000. In case the policyholder is caught up with a terminal or critical illness, the insurance company will pay a lump sum amount for the medical expenses.

Therefore, life insurance provides much-needed financial assistance to the family members of the insured person in the event of emergencies.

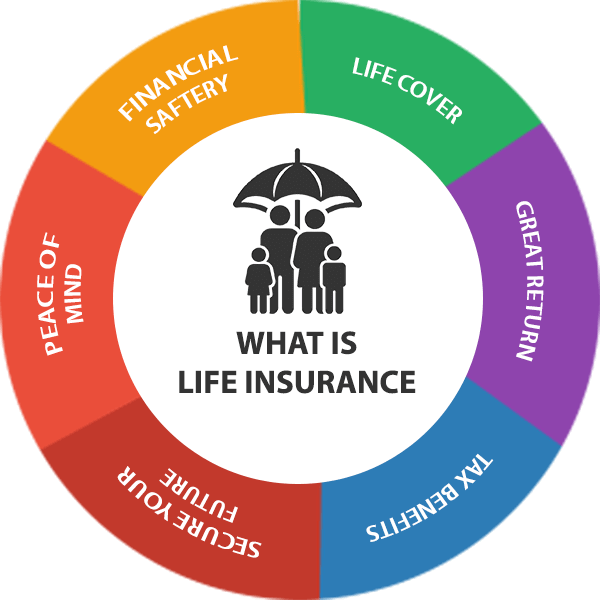

Individuals can safeguard themselves and their families with life insurance in the event that something bad happens to the insured. The insurer pays an amount equal to the sum assured as indicated in the contract, plus any incentives that may be available.

There are some life insurance policies that offer two lucrative benefits of both insurance and investment. This simply means that one part of your premium goes towards insurance and the other part is invested in debt, equity, etc. With a strong protective covering and higher returns on your investments, you certainly get the best of both options.

A life insurance plan also acts as a saving instrument by providing maturity benefits. In case the policyholder lives to the end of the policy term without any claims, the total amount of premiums is refunded at the policy’s maturity time. For example, if you pay a yearly premium of Rs. 10,000 for a 30-year term insurance policy, you would receive the premium money back (Rs. 3,00,000) along with the bonus amount. This is only when you survive the policy tenure and you have paid all of your premiums.

Tax saving is an additional benefit when it comes to purchasing a life insurance plan. As per Section 80C of the Income Tax Act, 1961, you will be subjected to get tax benefits. Simply putting, whatever premium amount you pay for your life insurance policy, it is eligible for having a maximum tax deduction of up to Rs. 1,50,000. Besides, any payouts that you will receive from your life insurance policy will be entirely tax-free under section 10(10D). In case you have chosen for an additional health-associated rider, you are subjected to avail tax deductions under Section 80D of the Income Tax Act.

Be it your children’s education loan, credit card loan, building capital for your business, or retirement plan, dealing with such kinds of liabilities can lead to great financial as well as mental pressure. And when there is no steady source of income, such liabilities can prove even more challenging. Therefore, in order to attain your important goals, you need a significant amount of financial support that life insurance can easily provide.

Life insurance policy comes with a multitude of riders, such as Critical Illness Rider, Accidental Death Rider, Cashless Treatment Rider, etc. They provide extra protection to the individuals as well as their family members in cases where basic life insurance coverage may not come into play or need.

Smart investors constantly search for financial products that deliver both safety and growth potential. The Securities and Exchange Board of India (SEBI) is developing an

Life is unpredictable, and sometimes, even the best-laid plans can get interrupted by unforeseen circumstances—job loss, medical emergencies, or sudden financial strain. When this happens,

In a world buzzing with anticipation and joy, you’re a couple who found themselves on the thrilling journey of pregnancy. Each flutter of movement brought